By Mike Murphy 12/04/2017

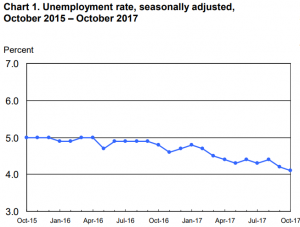

As the U.S. economy continues to improve, so does the demand for labor. According to the Bureau of Labor Statistics, the current unemployment rate has edged down to 4.1 percent. Many economists maintain that demographic trends will continue to contribute to a greater shortage of qualified labor. Small business owners will be hit hardest by this trend, making it more important than ever to put effort into attracting and retaining qualified employees.

After pay scale, prospective employees are more likely to inquire about benefits than any other topic. Small business owners are finding that offering a retirement plan, such as a SIMPLE IRA or 401(k), is becoming a necessity to compete for quality employees.

There is good news for small business owners. Not only does offering a qualified retirement plan benefit your employees, it also comes with large tax perks for you as the owner. Depending on the type of plan you put in place, you, as owner, can defer over $350,000 in pre-tax earnings per year. The IRS also allows the business to deduct expenses associated with the administration of the plan.

Some retirement plans, such as 401(k), allow the business to impose vesting schedules to aid in employee retention. A vesting schedule requires employees to work at the business for a specified period of time before they have full rights to the money you have contributed into their account. One of the most common vesting schedules requires six years of employment before the full account value can be released. Employees who terminate sooner are able to withdraw all money that they have contributed, but will forfeit a portion of the employer-contributed funds.

If you’re looking to add a benefit while keeping costs to a minimum, a different type of plan design may be more appropriate. It’s possible to put a plan in place that provides tax benefits to your employees without requiring employer contributions.

The key to finding the right plan for your needs lies in evaluating your current business structure, goals, and cash flow. Consider your employment needs, current employee turnover rates, and the degree to which the business will participate in the plan. This information is used to select the appropriate plan type and determine the specific details of plan design.

Once your plan is in place, it’s important to inform current and future employees about the benefit. Regular education and enrollment meetings will help to encourage participation.

It’s not uncommon for business owners to find this process daunting. However, the benefits of offering a qualified retirement plan far outweigh the effort. Working with a qualified retirement plan specialist can help ensure proper plan design, simplify the implementation process, and ensure that your plan continues to be a benefit, rather than a burden.

Mike M urphy is vice president of ERISA consulting at FiduciaryShield a retirement plan fiduciary administrator and compliance company.

urphy is vice president of ERISA consulting at FiduciaryShield a retirement plan fiduciary administrator and compliance company.

Topics: #401(k) #Retirement #retirementplans #benefits #employeeretention

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

CONNECT WITH US